Deliver Seamless Customer Onboarding With Creatio

In today's world, banks offer a variety of financial products and services – like savings accounts, loans, credit cards, and more. But let's be honest, the rules and how everything works in the world of banking can be pretty confusing, especially if a customer is new to it all.

For newbies to start their banking journey smoothly, banks have developed a special strategy. It’s known as "customer onboarding," and it serves as a welcoming companion that assists in navigating the occasionally complex world of banking. In reality, it stands as one of the pivotal responsibilities of banks, as it revolves around delivering the utmost convenience and support to customers, striving to offer the most favorable customer experience possible.

Let's explore customer onboarding in more detail and see why it matters so much in the banking industry.

Why is Customer Onboarding Important for Banks?

Customer onboarding in banking is a crucial process because it sets the stage for successful and long-lasting customer relationships. Even though customer onboarding procedures can vary among different banks, their shared objective remains unchanged: to facilitate a quick and effortless start for customers in using banking products and services. By ensuring a smooth start, onboarding ultimately leads to higher customer satisfaction, reduced customer churn, and increased profitability, all while helping the bank meet legal requirements and minimize the risk of fraud.

Let's take a closer look at some of the key reasons why banks prioritize customer onboarding:

- First impression advantage. Customer onboarding in banking allows for making a favourable first impression and equips new customers with the knowledge necessary to use banking products and services with ease.

- Value realization assurance. Effective onboarding ensures that customers realize the value of the bank's products and services, which reduces the likelihood that they may switch to another bank.

- Loyalty-driven growth. Happy, loyal customers are more likely to use additional banking products and services, which boosts the bank's revenue and profitability.

- Compliance confidence. Customer onboarding assists banks in verifying the identity of customers and collecting the information required to comply with laws and regulations, thereby preventing legal issues.

- Fraud risk mitigation. By carefully verifying customer information during onboarding, banks can lower the risk of fraudulent activities, protecting both the bank and its customers from potential harm.

Traditional vs. Digital Customer Onboarding in Banking

Customer onboarding in a bank can take two primary forms: traditional and digital. Traditional onboarding involves in-person visits to a physical branch, extensive paperwork, and manual processes, which can be time-consuming and less convenient for customers. In contrast, digital onboarding leverages technology to enable customers to open accounts remotely, offering greater accessibility, speed, and efficiency.

Drawbacks of the traditional approach

Traditional customer onboarding methods in banks are associated with several challenges, including:

Limited accessibility

Customers need to physically visit bank branches during working hours for in-person onboarding. It can cause you a great deal of inconvenience if you reside far from a bank location and also have a busy work schedule.

Time-consuming processes

Traditional onboarding methods often involve a plethora of paperwork, manual data entry, and in-person visits, making the process time-consuming for both customers and bank staff. This leads to delays in account activation and a less efficient customer experience.

According to a McKinsey report, know-your-customer (KYC) due diligence and account opening take up more than 40% of onboarding time for banks.

Documentation errors

Physical documents and forms can have mistakes, omissions, and handwriting that is difficult to read. These mistakes can lead to compliance issues, customer frustration, and the need for time-consuming manual corrections, which can be costly for the bank.

Security risks

Handling physical documents and paper-based processes poses security risks. Documents can be lost, damaged, or stolen, potentially leading to identity theft or fraud. Traditional methods also rely on manual identity verification, which may be less secure compared to digital methods like biometrics or two-factor authentication.

Inefficiency and high operational costs

Traditional onboarding requires significant human intervention and resources, including staff to review and process documents. This results in high operational costs for banks, which may be passed on to customers or affect the bank's profitability.

Positive aspects of going digital

Digital technologies, on the other hand, have made it possible to reshape this process by offering enhanced efficiency, cost savings, and the ability to cater to the preferences of demanding consumers. Here are some of its fundamental advantages:

Enhanced customer experience

Digital onboarding often provides step-by-step guidance and a user-friendly interface, making it easier for customers to understand and complete the process. As a result, customers have a better overall experience, which lowers the risk of applications being abandoned.

Convenience and accessibility

Digital onboarding allows customers to open accounts and complete the onboarding process from the comfort of their homes or on-the-go. This accessibility eliminates the need for physical branch visits, making it more convenient for customers with busy schedules or those who live far from bank branches.

Efficiency and speed

Digital onboarding streamlines the process by reducing paperwork and manual data entry. Customers can submit their information and documents electronically, leading to faster account activation and reduced processing times.

Improved accuracy

Digital onboarding reduces documentation errors by minimizing the need for manual data entry and physical paperwork. Customers can submit their information electronically, which is then automatically processed and validated, reducing the risk of errors caused by illegible handwriting or data entry mistakes. Additionally, digital systems can flag inconsistencies or missing information in real-time, prompting users to correct and complete their submissions, further reducing documentation errors.

Enhanced security

Digital onboarding methods can incorporate advanced security measures such as biometrics, two-factor authentication, and encryption, making it more secure than traditional methods reliant on physical documents. These security features protect customer data and reduce the risk of identity theft and fraud.

Reduced operational costs

Digital onboarding reduces the need for extensive physical infrastructure and manual labor, leading to lower operational costs for the bank.

The winner is clear

Traditional Onboarding | Digital Onboarding | |

|---|---|---|

| Accessibility | Typically, in-branch or paper-based, requiring physical presence. | Available online 24/7, accessible from anywhere with an internet connection. |

| Convenience | Time-consuming, involving paperwork and manual processes. May require multiple visits to the bank. | Faster and more convenient, allowing customers to complete the process remotely in minutes. |

| Documentation | Requires physical documents, photocopies, and signatures. | Accepts digital documents, scans, and e-signatures, reducing paperwork. |

| Identity verification | Often relies on in-person verification, leading to delays. | Utilizes digital identity verification methods, such as biometrics and document scanning, for real-time verification. |

| Customer experience | Can be less user-friendly and frustrating due to paperwork and wait times. | Offers a smoother and more user-friendly experience, enhancing customer satisfaction. |

| Compliance and security | Compliance checks may be manual, leading to potential errors. Security may be compromised due to physical documents. | Incorporates automated compliance checks and encryption, enhancing security and reducing fraud risks. |

| Cost Efficiency | Higher operational costs due to paperwork, physical infrastructure, and staff requirements. | Typically, lower operational costs due to automation, reduced paperwork, and fewer in-person interactions. |

Key Components of Effective Customer Onboarding in Banking

Customer onboarding processes may vary across different banks, but they all share a common set of essential components. These key components are vital for ensuring successful and efficient onboarding experiences that meet the diverse needs of customers.

Clear communication

Effective communication is fundamental. Banks should provide customers with clear and comprehensive information about the onboarding process, products and services, account terms, and required documentation. Clarity ensures that customers have a full understanding of what to expect during onboarding.

Digital accessibility

Accessibility through digital channels is essential. Banks should offer user-friendly mobile apps, websites, and online portals that simplify the onboarding process, making it easy for customers to open accounts, submit documents, and manage their banking digitally.

Streamlined processes

Streamlining processes reduces complexity and saves time. Automation of tasks like account opening, identity verification, and document submission speeds up the onboarding process, resulting in a more efficient experience for customers.

Security measures

Ensuring the security of customer data is of utmost importance. Banks should implement robust security measures such as encryption, multi-factor authentication, and fraud detection systems to safeguard sensitive information and protect customers from potential threats.

Multi-channel support

Customer support must be available through various channels, such as phone, email, live chat, and in-person assistance. This ensures that customers can access help and assistance in a way that suits their needs, enhancing their overall onboarding experience.

A Glimpse into the Future

Cutting-edge technologies like generative AI and the rise of "no-code" development tools are causing a big change in the way banks onboard new customers in the future. These technologies are paving the way for an onboarding process that is more efficient, flexible, and customer-focused.

Generative AI holds the potential to significantly enhance the customer onboarding process in banking. Firstly, it can analyze customer data to offer highly personalized services, including tailored financial advice, product recommendations, and real-time issue resolution. Secondly, it automates routine tasks, freeing up human resources for more complex matters, thereby increasing efficiency and reducing costs. This automation operates 24/7, ensuring customers have access to support whenever they need it. Lastly, generative AI provides a conversational banking experience, simplifying operations and making banking accessible to a global audience, transcending language barriers. In essence, generative AI streamlines onboarding, enhances customer service, and makes banking more convenient and inclusive.

A McKinsey study says that current generative AI technologies hold the potential to automate tasks that currently consume 60 to 70 percent of employees' time.

No-code platforms will empower banks to take control of their digital transformation. With these platforms, non-technical staff can create customized onboarding workflows without the need for extensive coding. This agility is crucial in adapting to regulatory changes, rapidly evolving customer preferences, and market shifts. It allows banks to design and implement onboarding processes efficiently, making adjustments on-the-fly, and ultimately reducing the time and costs associated with traditional development methods.

Gartner expects that by 2026, at least 80% of low-code development tool users will be outside traditional IT departments, up from 60% in 2021.

Streamline Customer Onboarding with Creatio

Investing in a cutting-edge software solution is a crucial step to facilitate effective customer onboarding in banking. The primary attributes of this solution, including its technological maturity, flexibility, user-friendliness, and cost-effectiveness, work together to streamline the customer onboarding process and keep the bank competitive in an ever-changing financial landscape.

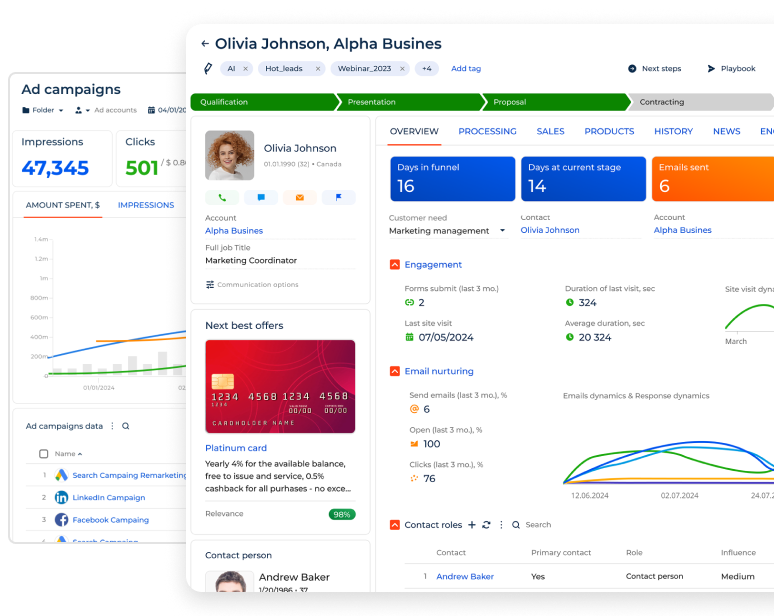

Creatio is an excellent example of such a solution. It serves as a comprehensive no-code platform, allowing banks to automate workflows and enhance customer engagement while enjoying maximum flexibility. With Creatio, banks can deliver not just personalized and exceptional onboarding experiences, but also optimize various front-office and middle-office processes, spanning marketing, sales, lending, verification, underwriting, compliance management, customer service, and more – all contained within a single solution.

FAQ

What is customer onboarding in banks?

Customer onboarding in banks refers to the process of welcoming and integrating new customers into the banking system, including opening accounts, verifying identities, and introducing them to available products and services.

Why is efficient customer onboarding important for banks?

Efficient onboarding enhances customer satisfaction, reduces the risk of fraud, ensures regulatory compliance, and streamlines internal operations.

How long does the typical customer onboarding process take in banks?

The duration varies but can range from a few hours to several days, depending on the complexity of the customer's needs and the bank's processes.

What technology is used to optimize customer onboarding in banks?

Banks often use digital solutions, including document verification, electronic signatures, and workflow automation, to streamline and digitize the onboarding process.

How can banks ensure data security during customer onboarding?

Banks employ robust security measures, including encryption, multi-factor authentication, and compliance with data protection regulations, to safeguard customer data throughout the onboarding process.

What is KYC in customer onboarding?

KYC, or Know Your Customer, is a regulatory process in customer onboarding that involves verifying the identity and background of customers to prevent financial crimes and ensure compliance with anti-money laundering (AML) regulations.