Digital Transformation in Banking: Strategy, AI Technologies, and Real-World Examples

Modernize Banking Ops with Creatio’s AI platform

The world is already digital-first. You can pay for groceries, order food, or book a ride—all from your mobile phone in seconds. Banking is expected to work the same way.

Traditional banking models — built on legacy systems and manual processes — are no longer sustainable in an environment driven by AI and automation. Banks are under increasing pressure to keep pace with rising customer expectations for seamless digital interactions, real-time services, and consistent experiences across mobile, web, and in-branch channels.

In this article, we explore digital transformation in banking — what it means, why it matters, the technologies driving it, and how financial institutions can get it started.

Key Takeaways

- Banking organizations must modernize legacy infrastructure to meet evolving regulatory needs, customer expectations and rising competition across the industry.

- Digital transformation results in a reduced cost-to-income ratio, faster process execution, higher employee productivity, with improving risk and fraud control

- Some of the popular applications of digital banking transformation include digital customer onboarding, automated loan origination, real-time AI fraud detection, and service excellence support and mobile-first banking.

- AI and autonomous agents are now key enablers of transformation, powering data analytics and real-time decision-making, and automating end-to-end customer lifecycles from acquisition to retention.

- Platforms like Creatio help banks and financial institutions accelerate digital transformation through an AI-native CRM and workflow automation platform where people and AI agents work together — streamlining banking operations, improving customer experiences, strengthening compliance, and scaling innovation across the business.

What is Digital Transformation in Banking?

Digital transformation in banking is the strategic adoption of digital technologies, data, and intelligent automation to redesign banking operations, services, and customer engagement. It enables banks to modernize legacy infrastructure, rethink end-to-end customer journeys, and support real-time, data-driven decision-making using modern technologies such as AI, cloud computing, and workflow automation.

While many banks have already digitized individual services — such as online banking or mobile apps — digital transformation is broader and more strategic. It involves redesigning the entire banking model, shifting from traditional systems to digital-first, data-driven, and automated operations that deliver more efficient, scalable, and customer-centric services.

Why Digital Transformation Is Important for Banks?

Digital transformation is not new to banking — it is already embedded in everyday services such as mobile apps, digital payments, online account management, and self-service portals. However, with the rising competition from fintechs and neobanks, traditional banks face growing pressure to keep pace by launching new services, operating faster and delivering superior user experiences.

Customer expectations are rising just as quickly. Users now demand seamless, real-time, and consistent experiences across mobile, web, and in-branch channels. Meeting these expectations requires banks to rethink the entire customer journey, ensuring it is secure, connected, and highly personalized.

At the same time, legacy systems and data silos limit the scalability and efficiency of banking operations. Many banks struggle to unify data, coordinate workflows, and maintain a complete customer view. All these challenges become the key drivers for exploring new digital technologies that modernize banking operations, orchestrate processes end-to-end, and deliver more connected, intelligent customer experiences.

Key Technologies Driving Digital Transformation in Banking

Digital transformation in banking is powered by a combination of technologies that enable banks to modernize infrastructure, automate operations, and deliver more connected customer experiences. These include:

Artificial Intelligence (AI) and Machine Learning

AI has evolved from an emerging capability to a core technology driving transformation in banking. Combined with machine learning, it enables institutions to automate decision-making, optimize operations, and deliver personalized services across multiple areas:

- Cybersecurity and fraud detection – AI identifies unusual patterns and anomalies in real time, helping detect fraud, malware, and phishing attempts. According to an Economist Intelligence Unit (EIU) survey, nearly 58% of banks use AI primarily to identify fraud.

- Risk management - AI models assess market volatility, geopolitical risks, and credit exposure, enabling more accurate and proactive risk mitigation.

- Credit scoring and underwriting – AI helps bankers analyzes broader data sets to improve decision accuracy and accelerate approvals.

- Customer service (virtual assistants and chatbots) – Virtual assistants and chatbots provide instant, contextual support while reducing manual workload.

- Customer insights and personalization – AI enables tailored recommendations based on behavioral and transactional data.

More advanced banking use cases include autonomous AI agents that manage end-to-end processes — such as onboarding, case resolution, and compliance workflows — with human-in-the-loop control. According to Creatio’s State of AI Agents and No-Code report, 73% of financial services leaders consider AI agents critical or important for achieving their strategic goals within the next two to three years.

Cloud Infrastructure

Cloud infrastructure provides computing resources, storage, and runtime environments for banking applications. This enables banks to ensure scalable, flexible, and cost-efficient operations without heavy upfront investment.

With cloud, banks can scale infrastructure on demand, launch new services faster, and reduce reliance on legacy systems. Continuous updates and built-in integrations help banks ensure security, compliance, and faster innovation across the entire organization.

Banking APIs and Open Banking

Application Programming Interfaces (APIs) are essential for building flexible, modular banking architectures. They enable secure connectivity between internal systems, external partners, and third-party applications without rebuilding functionality from scratch.

APIs support open banking initiatives and embedded finance — for example, enabling customers to link their bank account to a payment or budgeting app and manage finances in real time from a single interface.

Data Platforms and Advanced Analytics

Modern data platforms enable banks to aggregate, process, and analyze large volumes of transactional, customer, and operational data across systems. These include data lakes, data warehouses, and real-time streaming environments.

By combining unified data with advanced analytics, banks can improve fraud detection and risk assessment, make data-driven decisions in real time, and deliver personalized products and services.

Identity and Access Management (IAM)

Identity and Access Management (IAM) enables banks to securely control access to systems, applications, and sensitive data. It ensures that only authorized users can access the right resources at the right time.

By combining authentication and authorization, IAM reduces security risks and supports compliance. Key capabilities include Single Sign-On (SSO), Multi-Factor Authentication (MFA), and Role-Based Access Control (RBAC), helping balance strong security with a seamless user experience.

Low-Code / No-Code

Low-code and no-code technologies enable banks to improve systems and deploy new workflows using visual designers and drag-and-drop interfaces. By reducing reliance on traditional development cycles, they accelerate digital transformation and speed up the delivery of new services. The recent benefit study by Nucleus Research demonstrated that financial institutions can accelerate workflow delivery by up to 70% using no-code platforms.

Many platforms also embed AI capabilities, allowing banks to design, personalize, and scale enterprise-grade no-code applications more efficiently. This supports continuous innovation while maintaining control, visibility, and performance across operations.

Internet of Things (IoT)

In banking, IoT enables real-time, context-aware interactions between customers, devices, and financial systems. Think of smartphones and wearable smartwatches that support device-based and contactless payments or ensure more secure authentication through connected devices.

IoT-generated data can also be integrated into risk models and fraud detection systems, providing additional behavioral and contextual signals to improve banking operations and strengthen security.

Blockchain and Distributed Ledger Technology (DLT)

Blockchain becomes more popular in banking due to its ability to enable secure, transparent, and tamper-resistant transactions across multiple parties. In banking, this technology is used for cross-border payments, smart contracts, and digital identity verification — helping streamline processes and enhance their transparency.

Real-World Examples of Digital Transformation in Banking

Across the banking sector, many processes still rely on manual work, fragmented legacy systems, and complex approval chains. Below, we’ve outlined some practical examples of how banks can transform operations with digital technologies.

#1. Digital Customer Onboarding

Traditional onboarding relies on manual data entry, document verification, and multiple approval steps, which often take days to complete. With digital transformation, this routine process becomes significantly faster and more efficient.

For example, banking institutions deploy autonomous onboarding agents, which collect and validate customer data, pre-verify documents, and organize applications for approval. This allows teams to accelerate the customer onboarding process, deliver consistent customer experiences, and reduce operational costs.

#2. Loan Origination and Processing Automation

Loan origination is one of the most fragmented processes in banking, often involving separate systems for applications, credit checks, document verification, and approvals. With digital banking transformation, these workflows are handled within a unified platform, where data flows seamlessly across systems.

For example, when a loan application is submitted, AI models can instantly assess credit risk, validate documents, and trigger underwriting workflows. The system routes the application to the right stakeholders, generates required communications, and tracks the process end-to-end — reducing delays and eliminating manual handoffs.

#3. AI Fraud Detection

Each year, fraud schemes like e-commerce scams, investment fraud, and business email compromise result in billions of dollars in losses for banks. According to KPMG’s global banking scam survey, more than half of respondents already have, or are developing, dedicated scam-prevention frameworks, with common measures including transaction blocking (91%) and account freezing (85%).

Traditionally, these controls rely on manual review and rule-based systems, which are costly and difficult to scale. With digital transformation, banks can adopt AI-driven systems to monitor transactions in real time, analyze behavioral patterns, and detect anomalies as they occur. For example, suspicious transactions can automatically trigger warnings, pause payments, or request payee verification, enabling banks to prevent fraud proactively rather than reacting after the incident.

#4. AI-Enhanced Customer Support

Digital technologies have significantly transformed customer support in banking, where teams handle a constant flow of service requests, transactions, and exceptions — many of which are repetitive and time-consuming.

Today, customer service is shifting toward unified, omnichannel experiences powered by AI and automated workflow orchestration. AI-enhanced copilots and virtual chatbots handle routine requests such as balance inquiries, transaction disputes, card blocking, or payment status checks. At the same time, more complex cases are captured, enriched with context, and routed to human agents. This enables banks to reduce service costs and improve efficiency, while customers benefit from faster, more accurate, and consistent support across all channels.

#5. Mobile-first banking experience

Instead of treating mobile as just another channel, banks now design experiences around mobile as the primary interface for end-to-end customer interactions, where onboarding, payments, and servicing are handled directly within a mobile banking app.

Common examples of mobile-first transformation in banking include:

- Instant account opening with online identity verification

- Mobile payments and transfers with immediate confirmations and alerts

- In-app account management for balances, transactions, and card controls

- 24/7 customer support delivered directly through the mobile banking app

These capabilities make banking services more efficient and accessible, enabling faster interactions, greater convenience, and more control for customers over their financial activities.

#6. Personalized Banking and Cross-Selling

According to Financial Brand, 74% of consumers across all generations want more personalized experiences from their financial institutions. In response, banks are actively adopting AI, machine learning, big data and advanced analytics to create a 360-degree view of the customer and unlock more relevant, customer-centric interactions.

For example, banking AI agents can analyze financial data and interaction history to identify customer needs and recommend next-best actions—such as suggesting savings or credit products or triggering timely communications, including renewal reminders or investment recommendations based on lifecycle events. By engaging customers at the right moment with relevant offers, banks can increase revenue and improve overall customer lifetime value.

#7. Compliance and Regulatory Reporting

Digital banking workflows improve transparency and support regulatory compliance by ensuring accurate, timely reporting of financial and risk data. Instead of manually consolidating data from multiple systems, banks can generate compliance-ready regulatory reports directly from real-time systems, with workflows enforcing required checks, approvals, and audit trails. Transaction monitoring can also be automated to flag potential compliance risks early, making reporting more consistent and easier to manage under evolving regulatory requirements.

Benefits of Digital Transformation in Banking

Despite strict regulations and legacy processes, banks can unlock significant value through digital transformation, improving efficiency, customer experience, and overall performance. Key benefits of digital banking transformation are:

- Reduced cost-to-income ratio: Streamlining operations and reducing manual work allows banks to lower operating costs while maintaining or increasing output. For example, Nucleus Research found that financial institutions can reduce technology costs by up to 30% by adopting agentic no-code platforms.

- Faster execution across core banking processes: Shorter onboarding, approval, and service cycles improve operational efficiency and enable banks to respond faster to customer and market demands.

- Higher customer satisfaction and retention: More consistent, faster, and personalized experiences strengthen customer relationships and reduce churn.

- Improved risk control and reduced fraud losses: Digital processes reduce human error and provide better visibility into transactions, enabling earlier detection of anomalies and more effective risk management.

- Better decision-making across the organization: Access to consistent, real-time data improves planning, forecasting, and operational decisions.

- Improved scalability without proportional cost growth: Digital solutions enable banks to build new and optimize existing business processes, launch new services, and expand operations without a corresponding rise in operational overhead.

- Higher employee productivity: Employees spend less time on repetitive tasks and more time on high-value activities. For instance, according to McKinsey, AI adoption can improve the productivity of credit analysts by 20–60% and accelerate decision-making by up to 30%.

Challenges of Digital Transformation in the Banking Industry

Alongside the benefits, banks must also address several challenges when implementing digital transformation initiatives:

- Legacy infrastructure complexity

Many banks still rely on outdated core systems that are difficult to update, integrate, and scale. According to CIO, 63% of banks still depend on code written before 2000. Modernizing these environments requires a strategic approach and often significant changes across systems, processes, and organizational structures. - Data silos and integration issues

In the banking sector, customer and operational data are often distributed across multiple systems, limiting visibility and making it difficult to build a unified view. Legacy architectures and fragmented workflows make integration complex, while strict regulatory requirements further constrain data access and real-time analysis. - Regulatory compliance requirements

Banks operate under strict and constantly evolving regulations. Ensuring that new processes meet compliance standards adds significant operational and technical complexity to the digital transformation journey. - Cybersecurity risks

As banks expand digital channels and integrate more systems, the attack surface increases: according to Statista, around 65% of global financial organizations experienced a ransomware attack in 2024. Protecting core systems and sensitive data therefore requires continuous investment in security, monitoring, and risk management. - Organizational resistance to change

Digital transformation often requires changes in processes, roles, and culture. Resistance from employees or leadership can slow adoption and limit the success of transformation initiatives.

With a well-defined strategy in place, banks can not only overcome these challenges and improve operational efficiency but also become innovators in the financial services industry — new services faster, adapting to market trends, and creating more value for their customers.

How to Implement Digital Transformation in Banking

Successful digital transformation in banking requires a structured, strategic approach that aligns technology adoption with business goals, operational processes, and regulatory requirements. Leading institutions continuously refine their digital strategy by testing new technologies, learning from real use cases, and scaling what works.

Here’s a clear step-by-step approach for integrating digital technologies in banking:

Step 1: Assess current systems and identify gaps

Evaluate core banking systems, workflows, and customer journeys to uncover inefficiencies such as long onboarding cycles, manual data entry, fragmented processes, and limited data visibility.

As part of this assessment, identify legacy systems that can be modernized, integrated, or replaced with more flexible, scalable technologies. The goal is not to add complexity, but to pinpoint where modernization will simplify operations, improve data flow, and enable more efficient, connected processes.

Step 2: Define clear objectives and ownership

Understand what exactly you want to achieve with digital transformation and define key performance indicators aligned with business priorities (i.e., faster customer onboarding, automated underwriting, or reduced operational costs). Assign clear ownership to stakeholders responsible for delivery, oversight, and outcomes.

Step 3: Prioritize high-impact use cases

To maximize the impact of digital transformation initiatives, focus on specific processes with the highest ROI and urgency — such as onboarding, loan origination, customer service, or compliance. This approach allows banks to deliver early results and build momentum before scaling the transformation processes across the organization.

Step 4: Build a roadmap and launch pilot initiatives

Once priorities are defined, create a phased roadmap for each use case, starting with pilot projects to validate impact and minimize risk. Use pilot results to refine your digital transformation approach before scaling across the organization.

Also, consider implementing automation and AI capabilities that can quickly improve execution across key domains without increasing headcount or cost. For example, autonomous banking workflows can accelerate customer onboarding, document management, and approval processes, while AI-enhanced systems are used to analyze customer data for credit decisions, risk assessment, and personalized recommendations.

Step 5: Scale and continuously optimize

Expand successful initiatives across the organization, monitor performance, and continuously refine processes based on data, feedback, and evolving business needs.

Remember, digital transformation is not a one-time initiative; it’s an ongoing process of optimization. Banks that succeed take an iterative approach: experimenting with new technologies, validating use cases, and scaling solutions that deliver measurable value.

To support this journey, Creatio has introduced the Agentic Banking Blueprint — a practical guide for banking leaders on where AI agents can drive the greatest impact, how to evaluate and prioritize use cases, and how to scale adoption securely and efficiently across the organization.

— responsibly, measurably, and at scale.

How Creatio Supports Digital Transformation in Banking

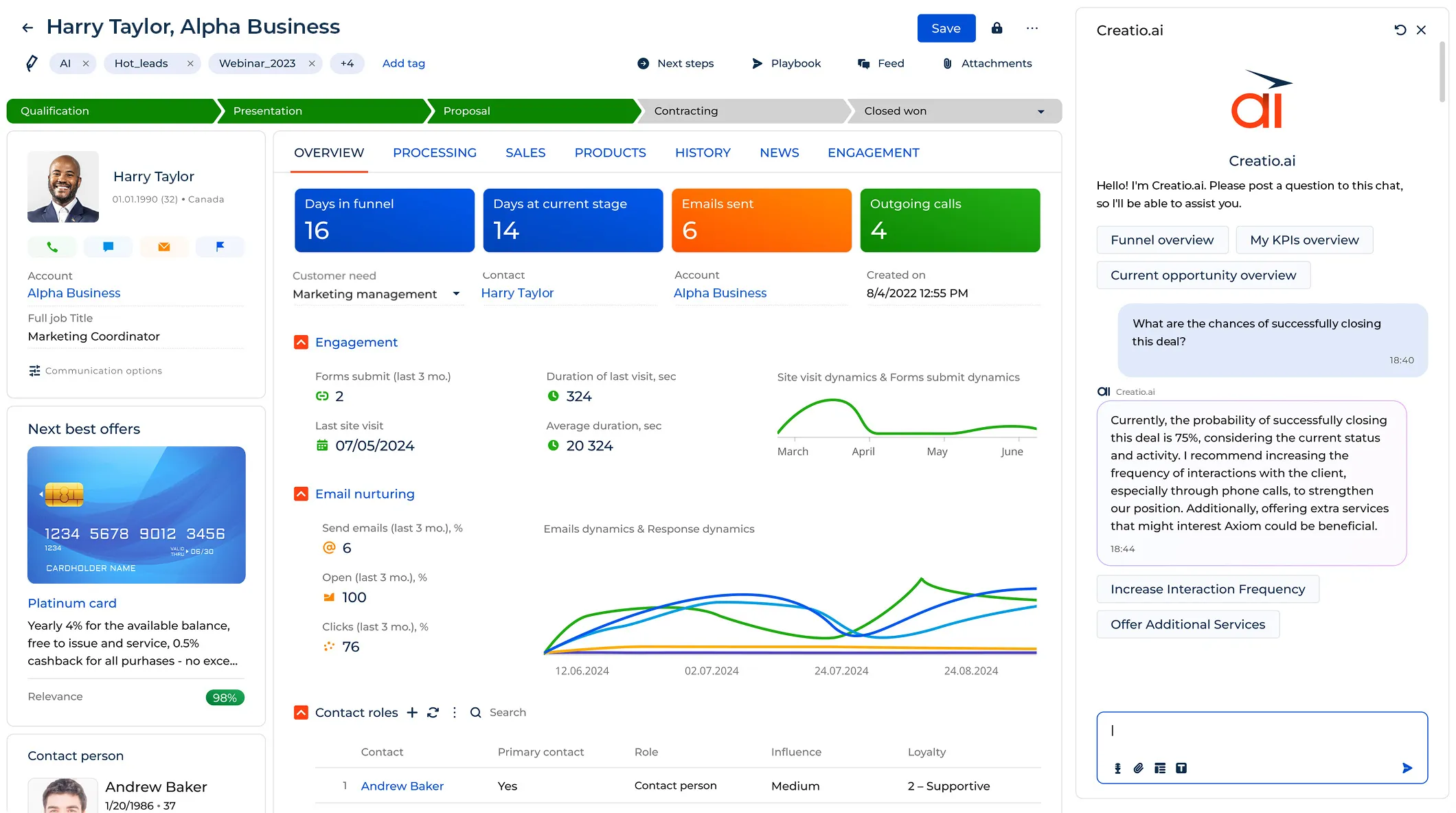

Creatio enables banks to execute digital transformation at scale by combining CRM, workflow automation, and AI into a unified, no-code platform. It empowers financial institutions to design, run, and continuously optimize end-to-end banking operations — across the entire customer lifecycle and product portfolio, including deposits, lending, credit cards, mortgages, wealth, and insurance.

Creatio’s AI CRM and workflow platform for banking

Built on a composable, AI-native architecture, Creatio allows banks to orchestrate processes across departments, systems, and channels. Its visual no-code tools empower teams to deploy new workflows faster, fully aligned to regulatory changes and operational needs.

Creatio embeds intelligent automation directly into banking and credit union operations through autonomous AI agents. These agents can identify opportunities, trigger next-best actions, and execute routine workflows with human-in-the-loop control — allowing banks to increase team productivity, improve customer experience, and reduce operational costs. The platform also enables banks to build custom AI agents tailored to their specific processes and regulatory requirements.

Creatio’s Core Features for Banking:

- End-to-end workflow orchestration customer lifecycle, product fulfillment, servicing, and compliance

- 360° customer view for more informed, personalized engagement

- Enterprise-grade security and governance, including RBAC, data encryption, audit trails, and compliance alignment)

- Seamless integrations with core banking and financial systems, plus access to the Creatio Marketplace with ready-to-use apps and templates

- AI-enhanced no-code development to rapidly build, customize, and scale banking applications and processes without heavy development cycles

Creatio’s AI and Agentic Capabilities for Banking:

Creatio applies AI-native automation as a force multiplier for banking teams. It automates routine tasks, generates predictive insights, and coordinates workflows across systems, with human oversight built in for regulated decisions.

Pre-built autonomous agents help banks improve revenue operations and drive efficiency, including:

- Referral Agent – identifies and tracks cross-sell opportunities

- Renewal Agent – monitors renewals and guides personalized offers

- Retention Agent – detects churn risks and initiates retention actions

- Customer Onboarding Agent – validates data and accelerates approvals

- Loan Preparation Agent – structures applications and checks eligibility

- Loan Servicing Agent – automates servicing and customer updates

Creatio’s autonomous agents can operate independently, coordinate across workflows, and work directly within tools such as Microsoft Teams, Outlook, and Zoom. This enables faster time-to-value, higher ROI, and lower total cost of ownership compared to traditional systems.

Top 3 Trends in Banking Digital Transformation

To better understand where the industry is heading, here are the key trends shaping digital transformation in banking:

1. Autonomous Agents for Banking

Autonomous agents are now emerging as a foundational shift in how banking operations are executed. They address a long-standing challenge in banking — fragmented processes across systems, teams, and channels — by introducing a consistent, governed execution layer that operates across these boundaries.

Unlike banking automation, autonomous agents are outcome-oriented systems: monitor events, apply business rules, initiate actions, and orchestrate multi-step workflows across systems.

Rather than providing insights and recommendations, these agents execute defined tasks within risk thresholds and escalate exceptions to human agents when needed. In the banking industry, it enables institutions to reduce reliance on manual coordination while strengthening control and accountability.

Autonomous agents can support and optimize every stage of the customer lifecycle:

- Acquisition — identify high-intent prospects based on behavioral signals, trigger outreach campaigns, and qualify leads automatically

- Onboarding — validate customer data, pre-check documents, and route applications for approval to reduce onboarding time

- Expansion — detect spending patterns or lifecycle events and trigger personalized product offers (e.g., credit, savings, insurance)

- Referral — identify satisfied customers, prompt referral requests, and track referral conversions automatically

- Retention — monitor engagement and transaction patterns to detect churn signals and trigger retention actions

- Renewal — track upcoming renewals, generate personalized offers, and initiate outreach before contract expiration

- Win-back — identify inactive customers and trigger targeted campaigns with tailored incentives to re-engage them

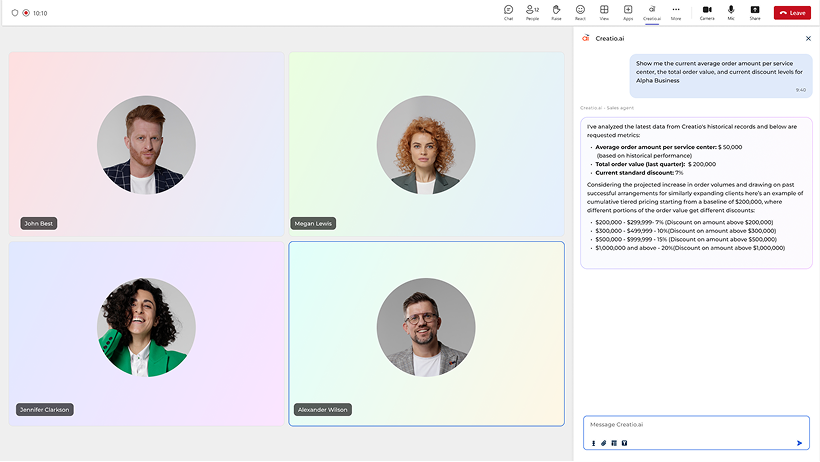

Example: Optimizing Customer Lifecycle with Autonomous Agents

2. Cloud migration

Cloud adoption is increasing across the banking sector as institutions modernize infrastructure to improve scalability and support evolving digital services. Today, many financial institutions have already established cloud programs. According to McKinsey’s European Digital Banking Survey, banks plan to increase the share of applications running in the cloud, from around 30-40% today to up to 70% within the next three years.

One of the key drivers of this shift is the growing use of data-intensive technologies, including AI. As banks adopt platforms with embedded AI capabilities or experiment with agentic automation, they require infrastructure that can handle variable workloads and large data volumes. Cloud environments provide the flexibility to support these use cases and scale resources as needed, without relying solely on on-premises systems.

3. Hyperpersonalized CX

Customer expectations have shifted from generic service to real-time, individualized engagement. Today, customers expect their bank to understand their needs, anticipate intent, and respond instantly through relevant product offers, financial guidance, or proactive support.

The “hyperpersonalized customer experience” trend means delivering even more relevant interactions — such as tailored product recommendations, dynamic pricing, or timely financial advice — based on a customer’s current context and behavior. By combining transactional, behavioral, and contextual data, banks can deliver the right message, product, or decision at the exact moment it matters, across every touchpoint.

Looking ahead, hyperpersonalization will play a critical role in improving retention, increasing product adoption, and driving revenue growth, setting a new standard for customer experience in banking.

Summary

Digital transformation in banking is about moving from slow, fragmented processes to connected, real-time operations. Banks that modernize their systems, unify data, and automate workflows can execute faster, make better decisions, and deliver more relevant customer experiences.

Creatio enables banks and credit unions to accelerate digital transformation with the best-in-class CRM and workflow platform, powered by generative, predictive, and agentic AI. It helps institutions design and run end-to-end processes, embed AI into daily operations, and scale digital transformation faster.